Vaishalee Bharadva

Posted on March 21, 2025

Building More Reliable Credit Models

with AA-Verified Income

For years, India’s lending industry has prioritized speed—fast approvals, seamless onboarding, and instant disbursals. However, this rapid expansion has exposed critical flaws in risk assessment, leading to rising defaults and worsening Non-Performing Assets (NPAs).

The Need for Reliable Income Assessment

Traditionally, lenders have relied on imputed income models to evaluate a borrower’s repayment capacity. These models estimate income based on credit history, loan size, and spending patterns. While efficient, they are built on assumptions rather than actual financial data. As a result, they often overestimate repayment capacity, leading to inflated loan approvals and increasing delinquencies.

The shortcomings of this approach are now evident—NPAs in unsecured retail loans surged to 4.5% as of mid-2024, nearly double the previous year’s levels. To enhance risk assessment, lenders need a more reliable way to verify income, based on actual financial transactions rather than inferred estimates. This is where Account Aggregators (AA) play a crucial role.

Why Traditional Bureau-Based Income Estimation Falls Short

Bureau-based income models have long been the foundation of digital lending, particularly for personal loans, Buy Now Pay Later (BNPL), and credit cards. However, their limitations are becoming increasingly evident:

- Assumption-Based Credit Decisions – Income is inferred from loan history, credit limits, and spending behavior, which fails to account for gig workers, freelancers, and MSMEs with irregular earnings.

- Limited Financial Visibility – Bureau data excludes savings, EMI obligations, and liquidity buffers, resulting in inadequate credit risk assessments.

Given these shortcomings, lenders must transition from assumption-based underwriting to fact-based income verification—this is where AA-based income estimation comes in.

AA-Based Income Estimation: A More Accurate Approach

The Account Aggregator framework enables lenders to access real-time, verified financial data directly from a borrower’s bank accounts, eliminating reliance on proxies and assumptions.

How AA Enhances Lending Decisions

- Accurate Income Verification – Instead of relying on indirect indicators, lenders can assess actual salary credits, business cash flows, and spending habits.

- Holistic Financial View – AA data provides a comprehensive picture of a borrower’s financial commitments, including savings, recurring liabilities, and outstanding EMIs.

- Regulatory Compliance & Data Security – Operates under RBI-approved financial data sharing framework, ensuring borrower control and privacy.

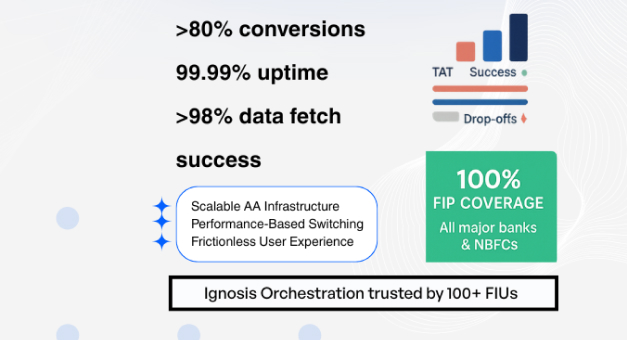

AA is already seeing rapid adoption—₹46,200 crore in loans were disbursed via AA in H1 FY25, highlighting its role in enhancing risk management and lending efficiency

The Conversion Rate Dilemma: A Short-Term Trade-Off for Long-Term Gains

Unlike bureau-based models, which function passively, AA requires explicit borrower consent, adding an extra step to the loan journey. This has raised concerns about lower conversion rates, but early trends suggest these fears may be overstated:

- 13% Monthly Growth Rate in cumulative successful consents, indicating that borrowers are increasingly comfortable with AA-based verification.

- Digitally-active NBFCs have been early adopters, leveraging AA to mitigate fraud risks and enhance credit quality.

As AA integration becomes more seamless, conversion rates are expected to stabilize while reducing NPAs and improving repayment performance. Lenders must recognize that while AA may initially lower approval rates, it significantly reduces risk exposure and strengthens portfolio quality.

How Lenders Can Transition Without Losing Volume

To implement AA-based income estimation without compromising loan volumes, lenders should adopt the following strategies:

- Hybrid Model Implementation – Use bureau data for pre-screening and AA for final verification to balance conversion rates and risk assessment.

- Customer Education & Trust Building – Address consent hesitancy by clearly communicating AA benefits, such as better loan terms and faster approvals.

- Seamless AA Integration – Ensure frictionless digital consent journeys to minimize borrower drop-offs.

- Shifting KPIs from Volume to Quality – Focus on portfolio health, NPA reduction, and repayment performance rather than sheer loan approval numbers.

Moving from Assumptions to Data-Driven Lending

India’s lending ecosystem can no longer afford to rely on inferred income models. AA-based income estimation is not just an enhancement—it is a necessity for sustainable, risk-mitigated growth.

While AA adoption introduces short-term friction, its long-term benefits—lower NPAs, improved risk profiling, and stronger borrower trust—far outweigh the costs. By embracing AA, lenders can build a more resilient, data-driven credit landscape that fosters responsible lending and financial inclusion.

Transform your lending with Account Aggregator verification, get in touch with us today!

Category 01

Indian financial compliance teams face a considerable challenge in managing employee investment

Nirav Prajapati

May 7, 2025

Read More

Category 01

Indian financial compliance teams face a considerable challenge in managing employee investment

Nirav Prajapati

May 7, 2025

Read More

Want these results for

your lending stack?

Book a Demo